Thanks to the advances of modern medicine and decades of public health research into longevity, living until 100 is now a real possibility for many people.

By adopting a healthy lifestyle that includes eating a balanced diet, keeping physically active, and getting enough sleep, you could boost your chances of living to a great age.

In fact, despite recent falls in life expectancy – due in large part to the coronavirus pandemic – new data published by A J Bell reveals that the number of centenarians in England doubled to more than 15,000 between 2002 and 2022.

While the prospect of a longer life might be enticing, it could affect your financial plans both now and in the future. So, read on to discover how to prepare financially for a 100-year life.

1. Factor your life expectancy into your retirement plans

According to research published by Canada Life, many people aged 50 and over underestimate how long they’ll live. This could potentially lead to a gap between retirement reality and expectations.

And yet, with the number of 100-year-olds on the rise, preparing financially for a lengthy retirement could become increasingly necessary.

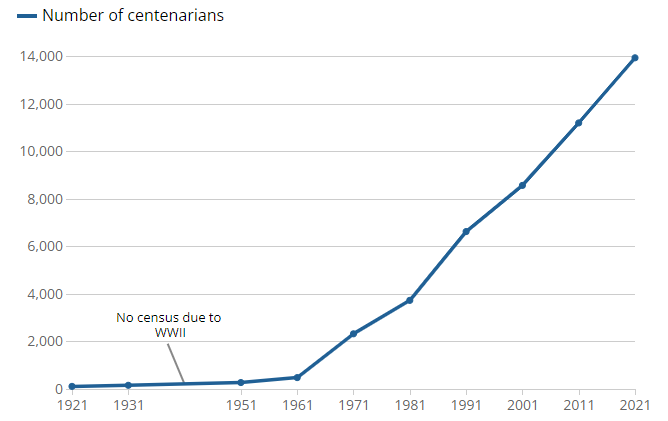

The below chart from the Office for National Statistics (ONS) shows the number of UK centenarians each year between 1921 and 2021. The sharp rise in the past 50 years is plain to see.

Source: ONS

If you’re fortunate enough to reach the age of 100, research published by MoneyAge suggests you might need an extra £240,000 in your pension pot – compared to a 65-year-old man living to their current average life expectancy of 84 years old – to achieve a comfortable retirement.

Of course, how much retirement income you’ll need will also depend on how you plan to spend your time.

But underestimating your life expectancy, or failing to factor it into your retirement plans altogether, could put you at risk of not saving enough to fund the lifestyle you want.

2. Consider how your retirement income needs may change over time

Your income needs probably won’t remain static throughout your retirement. So, factoring in a degree of fluctuation in your spending could help you prepare financially for a longer life.

It might be helpful to think about your spending in three stages that form a “retirement smile”:

- Active years – you might spend more during the early years of your retirement when you live out the big plans you’ve been dreaming about, such as travelling or renovating your house.

- Middle years – after the initial rush to make the most of your newfound freedom, you may begin to slow down and spend less. This could be a good opportunity to save.

- Later years – as you get older, your expenditure may rise to cover medical and care costs. According to Age UK, in 2023 it cost around £800 a week on average to live in a care home and £1,078 a week for a place in a nursing home.

A financial planner can use cashflow modelling to help you factor in the effect of the retirement smile when making your long-term financial plans.

3. Continue working for longer to boost your savings

Delaying your retirement and working for a few more years could allow you to continue growing your savings, including saving tax-efficiently into your pension. If you have a workplace pension, you’ll also benefit from ongoing employer contributions.

Indeed, working later in life is becoming more common. According to the Guardian, British workers are increasingly likely to work into their 70s.

If you do decide to delay your retirement, you might choose to leave your pension untouched for longer, giving it more potential to grow. Over time, the impact of compounding – earning interest on previous interest accrued – could have a powerful impact on the size of your pension pot.

The Lifetime Allowance

The removal of the Lifetime Allowance (LTA) charge, on 6 April 2023, means that you’ll no longer incur an additional tax charge if you exceed the previous LTA amount of £1,073,100.

So, if you previously stopped making pension contributions because you were nearing the LTA, it might be worth considering resuming payments.

Remember, though, that you’ll only be able to make contributions within your Annual Allowance – £60,000 to £10,000 (2023/24) – without facing an additional tax charge. Your Annual Allowance may be lower if your income exceeds certain thresholds.

Also, you might want to consult a financial planner to help you understand how much you can withdraw from your pension without incurring a heavy tax charge.

The Money Purchase Allowance

It’s important to note that if you do start making flexible withdrawals from your pension, this could trigger the Money Purchase Annual Allowance, which reduces your Annual Allowance from £60,000 to £10,000 (2023/24).

If you continue working for longer you could delay dipping into your pension pot and continue making tax-efficient contributions up to your full allowance.

4. Delay taking your State Pension

You don’t automatically receive your State Pension, you must claim it. If you don’t, it will automatically be deferred.

The benefit of delaying taking your State Pension is that you could receive higher payments when you do decide to claim it.

For example, if you reach State Pension Age after 6 April 2016, your payments increase by 1% for every nine weeks you defer. So, if you receive the full State Pension of £203.85 a week (2023/24), by deferring for 52 weeks, you’d receive an extra £11.82 a week or £614.64 a year.

5. Create a financial plan for drawing a tax-efficient and sustainable income

Having a financial plan is crucial when you enter decumulation – the process of drawing on your accumulated assets during retirement – and start to spend your wealth.

After spending years building your pensions, ISAs and other savings and investments, how you draw on your accumulated assets during your retirement requires careful consideration to ensure that your wealth lasts you for a 100-year life or longer.

A financial planner can help you structure a sustainable income by making the most of available tax allowances and exemptions, including:

- Income Tax allowances

- The Dividend Allowance

- Personal Savings Allowance

- ISA allowance

- Capital Gains Tax allowance

If you’re a couple, planning together and combining your allowances could help you to maximise your tax-free income.

6. Ensure your wealth is passed on tax-efficiently to loved ones

After working hard to accumulate and decumulate your wealth tax-efficiently over your lifetime, it makes sense to put an estate plan in place that ensures your loved ones receive as much of your wealth as possible after you’re gone.

If you haven’t planned how to pass on your wealth, your beneficiaries may have to pay more tax on their inheritance than they need to.

Inheritance Tax (IHT) is charged at 40% for estates worth more than £325,000 (2023/24). If you choose to pass on your main residence to direct descendants (children or grandchildren), you could benefit from an additional allowance of £175,000.

So, you could potentially pass on up to £500,000 without your beneficiaries needing to pay IHT, or up to £1 million if you and your civil partner or spouse combine your individual allowances.

However, IHT rules can be complex, so you might benefit from receiving professional financial advice.

7. Seek financial advice to help you plan for a 100-year retirement

Living longer means planning further ahead, which can be complicated.

A financial planner can use cashflow modelling to help you understand how much money you need to cover a lengthy retirement – including factoring in inflation, life expectancy, and fluctuations in your expenditure over time.

Get in touch

If you’d like help planning your long-term finances, please email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

Blue Wealth Ltd is not responsible for the accuracy of the information contained within linked sites.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pension Regulator.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

The Financial Conduct Authority does not regulate estate planning, cashflow planning or tax planning.