On 30 October 2024, chancellor Rachel Reeves announced a number of tax changes as part of her Autumn Budget.

One of the most significant – at least in terms of estate planning – was the inclusion of unused pension funds and death benefits in a person’s estate for Inheritance Tax (IHT) purposes.

Indeed, PensionsAge has reported that more than 150,000 estates may be affected by this amendment to current rules.

While this change is not due to take effect until April 2027, it could have important implications for your pensions and estate plan. As such, it’s worth getting to grips with the new rules and potentially, reconsidering how you want to pass on your wealth to loved ones.

Keep reading to learn more.

Pensions currently offer a tax-efficient way to pass on your wealth to loved ones

Your beneficiaries may face an IHT bill when they inherit your wealth if the value of your estate exceeds the following thresholds:

- £325,000 for most estates – This is your “nil-rate band”.

- £175,000 when passing on a home to your children or grandchild – This is your “residence nil-rate band”. Your residence nil-rate band may be reduced if your estate exceeds £2 million in total.

The government has frozen these thresholds at current levels until 2030.

You could combine these two IHT-free thresholds and pass on up to £500,000 tax-free – or up to £1 million as a couple.

Additionally, you can usually leave assets to your spouse or civil partner without triggering an IHT charge.

Any portion of your estate that you do not leave to a spouse or civil partner or that exceeds the IHT thresholds, is usually taxed at 40%.

However, under current rules, your pension is not considered part of your estate for tax purposes. As such, pensions can provide an effective way to pass on your wealth tax-efficiently.

Yet, it’s important to note that the Lump Sum and Death Benefit Allowance (LSDBA) limits the overall amount that your beneficiaries can take from your pension scheme without incurring a tax charge. This only applies if you die before you turn 75.

Inheritance Tax changes could result in a “double tax” on pensions

From April 2027, pensions will no longer be exempt from IHT. So, if your estate exceeds the tax-free thresholds, any unused pension savings will be included in IHT calculations.

According to figures from the UK government, this change could increase the average IHT bill by £34,000.

What’s more, if you pass away after the age of 75, your beneficiaries will pay Income Tax at their marginal rate when they draw from your pension.

This could mean that any pension savings you leave for your loved ones are diminished by a “double tax” – IHT and Income Tax.

So, if you’re currently relying on using your pension to help mitigate IHT, it might be worth reviewing your estate plan.

3 practical ways to address the planned Inheritance Tax changes

Fortunately, there are several ways you could mitigate a potential IHT bill, in light of the planned changes.

1. Gift some of your wealth during your lifetime

You could reduce the value of your estate and a potential IHT bill by gifting some of your wealth to loved ones during your lifetime.

In the 2024/25 tax year, you are entitled to the following gifting allowances and exemptions:

- Annual exemption – Allows you to gift up to £3,000 to one or multiple people. You can carry forward any unused exemption to the following tax year – but only for one tax year.

- Gifts for weddings or civil partnerships – You can give up to £5,000 to a child, £2,500 to a grandchild or great-grandchild, and £1,000 to any other person.

- Small gift allowance – You can give as many gifts of up to £250 each tax year as you wish (provided that you have not used another allowance on the same person).

- Gifting from surplus income – This rule allows you to pass on money from your income directly rather than gifting from savings. Theoretically, there is no limit to the amount you could gift in this way, although you must meet the strict criteria to qualify for this exemption – payments must be made regularly, you must be able to maintain a reasonable standard of living while giving the gifts, and your gifts should come from surplus income.

Beyond these annual gifting exemptions, most other gifts you give are likely to be “potentially exempt transfers” (PETs).

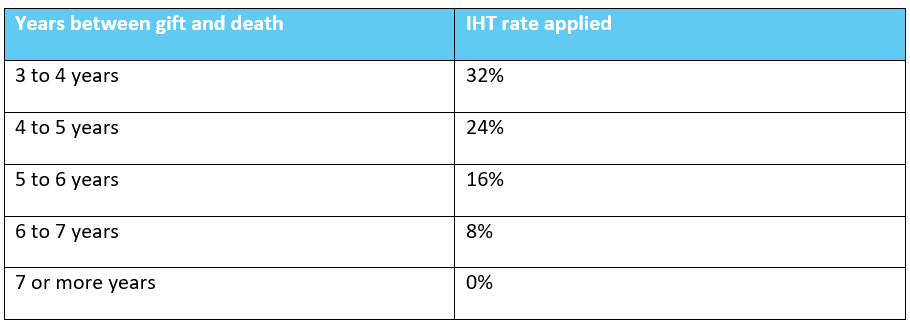

Any PETs will usually fall outside your estate for IHT purposes, provided that you live for more than seven years after giving the gift. However, if you die within seven years, taper relief rules may apply.

This means that the amount of IHT due will be calculated based on how soon you die after making the gift.

The table below shows how IHT relief tapers for PETs:

Bear in mind that PETs will be the first part of your estate assessed against your nil-rate band. So, if you die within seven years of making PETs that do not exceed your nil-rate band, there will be no taper relief.

2. Leave your pension to your spouse or civil partner

Any wealth – including pensions – you leave to your spouse or civil partner is usually exempt from IHT. So, passing your pension savings on to them could be an effective way to mitigate your IHT liability.

However, your pension will not automatically transfer to your spouse or civil partner when you die; you need to actively nominate them as a beneficiary.

You can usually do this by contacting your pension provider and completing an “expression of wish” or “nomination of beneficiaries” form.

If you have multiple pensions, it’s important to make arrangements with each provider to ensure that your spouse or partner benefits from your full pension entitlement.

You might also want to update any expression of wish forms you have completed previously, for example, if an ex-partner is named as a beneficiary.

It’s worth noting that while your partner or spouse may not incur an IHT charge if you pass your pension on to them, they will still have to pay Income Tax on any withdrawals they make if you die age 75 or older.

3. Place life insurance in a trust

Calculating your IHT liability and setting up a life insurance policy for this amount may provide invaluable peace of mind.

Your beneficiaries could use the insurance payout to cover a potential IHT bill, which may alleviate some of the stress and financial pressure they may otherwise experience after you’re gone.

What’s more, placing your life insurance in a trust could mean that the payout will not form part of your estate for tax purposes and as such, will not be subject to IHT.

Additionally, your loved ones may receive their inheritance more quickly, compared to going through the probate process which can take months or more.

Get in touch

If you’re concerned about the upcoming changes to IHT and pensions, we can help you review and update your estate plan.

Please email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

Blue Wealth Ltd is not responsible for the accuracy of the information contained within linked sites.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning or tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

Note that life insurance plans typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Cover is subject to terms and conditions and may have exclusions. Definitions of illnesses vary from product provider and will be explained within the policy documentation.

Approved by Best Practice IFA Group 11/02/2025