Investing small sums on a regular monthly basis allows you to drip-feed your money into the markets. Creating a habit to save little and often, over the long term, could make a big difference to your overall level of wealth.

Building your portfolio with regular top-ups to your investment portfolio using smaller amounts of money can also prove less risky and more profitable. This can make it particularly appealing during periods of high market volatility, as we have experienced in the first half of 2022.

Regular investing can be a great way to save for your children, too

Alternatively, if you want to save for a child’s future, investing regularly while children are growing up can help you to accrue a healthy lump sum. This can then be used to cover university fees, a deposit for their first property or an adventure, such as world travel or starting their own business.

Read more: How to invest wisely for your grandchildren

Here are five more reasons regular investing can be a useful way to grow your wealth.

1. Build discipline

Investing regularly helps you form a good savings habit and keep you committed to a long-term investment strategy.

Typically, the longer you leave your money invested, the greater the potential rewards.

For those new to regular investing, a good approach is to invest a fixed portion of income each month. Then, as your income fluctuates over your working life, you can simply adjust the amount you’re saving in line with the amount of money you are making.

Over time, no matter how little you might save each month, your regular investment should build up. It shouldn’t be long before you start to see a sizeable pot accumulate. This measure of achievement can help keep you motivated to keep topping up your investments.

2. Profit from compound growth

Compound growth is the most powerful and underrated benefit of long-term investment. It also has its largest impact during the latter stages of your investment journey.

For example, 10% growth on £1,000 is only £100, but 10% growth on £1 million is £100,000.

As these figures tell you, starting early and establishing a strong saving habit is vital if you want to reap the full rewards of compound growth.

Thanks to the effects of compound growth, even small sums add up and can help make a big difference later down the line.

To illustrate the power of compounding, if you invested £500 a month for just five years – from your 16th to your 21st birthday – in a fund that delivered 5% a year, and made no other contributions for the rest of your life, by your 60th birthday you’d have accrued almost £300,000 (The Calculator Site).

3. Bounce back from market dips sooner

Drip-feeding your money into the stock market means that you will be buying shares at a range of different prices.

When prices rise, your money will buy fewer shares. But, when prices drop, your money will go further and buy you more stock.

This is called “pound-cost averaging”.

Because pound-cost averaging can help to eliminate the impact of volatile markets, over time, you end up buying the average market price.

Also, If the market goes through a rough patch – as we have seen during the first half of 2022 – regular investing helps cushion the impact.

While there’s no guarantee of achieving better returns than you’d get from investing a lump sum, over a fixed, long-term period, you will end up paying the average price of the share. In effect, this reduces your risk and provides you with potentially smoother returns.

4. Pick up potential bargains

Many people find it difficult to remove emotion from investing and so struggle to benefit from market downturns. Helpfully, regular saving reduces this emotional element of investing.

For example, when stock market prices start to fall, some investors instinctively panic and avoid investing more money into the markets.

Nervous investors, who get spooked by market changes, may pull their money out of the market or refuse to enter the market until things settle down. And yet, because investors’ fear drives prices artificially low, this is often the best time to buy into the market.

At times like these, topping up your investment portfolio means that you may be primed to enjoy larger returns when the markets rally.

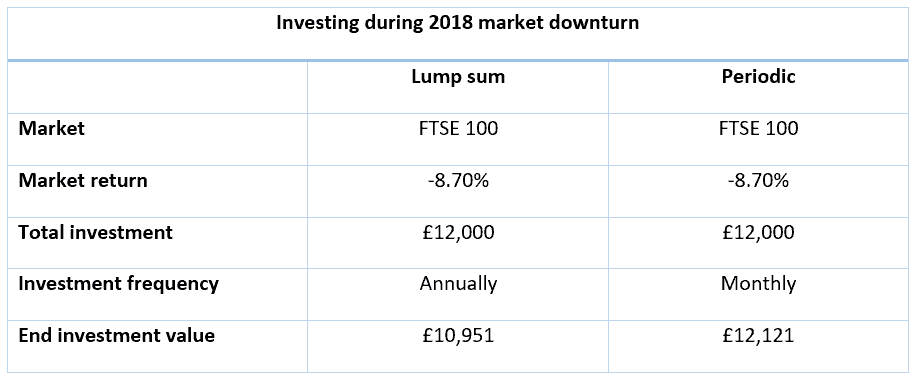

The table below shows how a regular £1,000 investment every month during 2018 compared with a £12,000 lump sum invested at the beginning of the year. In both cases, dividends are reinvested and don’t take fees into account.

Source: Bloomberg

5. Resist temptation to “time” the market

Some people will agonise over when they should invest their money in the stock market, hoping to find the perfect time to buy. However, there’s rarely such a thing as “perfect”.

Even professional investors and money managers with substantial sums to invest will drip-feed their funds into the market over time (usually over the course of a few months, depending on the circumstances).

As the strategy of seasoned professionals, it’s a great approach for novice investors, too.

Get in touch

Regular investing is a powerful discipline that you can use to build your wealth. The sooner you start, the better. We’ll help you identify what your dream future looks like and use financial modelling software to illustrate how regular investing can help you achieve your goals.

To find out more about how we can help you invest your money wisely and profit from long-term growth, email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note: The content of this newsletter is offered only for general informational and educational purposes. It is not offered as and does not constitute financial advice.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Naomi is our new trainee paraplanner. Arriving from another firm in Bristol, here she tells us a bit more about what she’s been up to since joining the team at Blue Wealth.

Naomi is our new trainee paraplanner. Arriving from another firm in Bristol, here she tells us a bit more about what she’s been up to since joining the team at Blue Wealth.

What is your background, can you tell us a bit about your journey to becoming a financial planner?

What is your background, can you tell us a bit about your journey to becoming a financial planner?