HM Revenue and Customs (HMRC) collected more than £4.6 billion in Inheritance Tax (IHT) between April and December 2021, £600m more than the same period in the previous year.

Meanwhile, the value of estates keeps climbing. A large part of the reason for this is the increase in house prices. According to research from estate agency Savills, 1 in 42 homes are now worth more than £1 million, and around 80% of new “property millionaires” are outside London.

As house prices and other asset values continue to rise, more families will fall victim to IHT.

The good news is that everyone has a tax-free amount

While IHT is due on everything you own when you die, the good news is that everyone has a tax-free amount, known as the “nil-rate band” (NRB). In 2022/23 the NRB allows you to give away £325,000 tax-free if you are single or £650,000 if you are married.

You might also be eligible for the residence nil-rate band (RNRB), which could boost your tax-free allowance to £500,000 for a single person or £1 million for a married couple, if you leave your home to children or grandchildren.

Anything above these thresholds is typically taxed at 40%.

Estate planning can help protect your wealth

An important part of the work we do with our clients is helping to preserve family wealth, ensuring it’s passed on to future generations, without being unnecessarily eroded by IHT charges.

Read on to find out five ways to protect your wealth from IHT liability.

1. Write a will

Without a will in place, your estate may be distributed in a way that doesn’t match your wishes. Helpfully, a will can also be used to help reduce IHT liability. For example, ensuring your main home goes to your child or grandchild can mean you’re able to use the RNRB, mentioned above.

In addition, if you leave at least 10% of the value of your estate to charity, you could reduce the IHT rate payable on your estate from 40% to 36%.

2. Use the gifting allowances

Gifting some of your wealth while you’re still around can be rewarding, as well as helping to reduce your estate’s liability for IHT when you pass away.

There are several gift exemptions you can make use of each tax year. The following gifts fall immediately outside of your estate:

- Up to £3,000 each tax year

- Up to £250 per person each tax year, as long as you haven’t used another exemption on the same transfer

- Wedding or civil ceremony gifts up to £1,000 per person, increasing to £2,500 for grandchildren and £5,000 for children and stepchildren

- Payments that help with another person’s living costs, such as an elderly relative or child.

On top of these, you could also use potentially exempt transfers (PETs), which allow you to give unlimited amounts to anybody you like. If you gift more than £3,000, you will not immediately be taxed. However, if you pass away fewer than seven years after making the gift, it will be subject to IHT.

Unlike the standard 40% IHT charge, PETs exist on a sliding scale, known as “taper relief”.

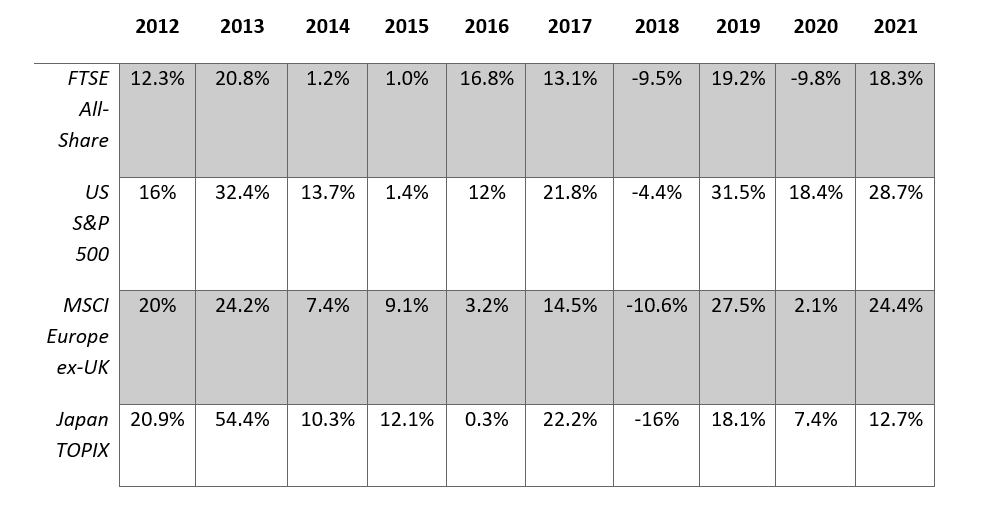

Source: HMRC

3. Make gifts from surplus income

You can also use surplus income to make gifts. For gifts to qualify, they must form part of your normal expenditure without harming your standard of living. If you decide to take advantage of this, it’s important to keep good records.

If you’re interested in gifting some of your wealth, or income, get in touch. We can help you understand how much you can afford to give away, without jeopardising your own financial situation.

4. Ringfence assets with a trust

Another useful way to pass your wealth without triggering an IHT charge is to establish a trust.

Trusts can be particularly useful when:

- You want to pass money to children or grandchildren but think they are too young to spend it wisely

- You wish the money to be used for a specific purpose, such as education, buying property, or another milestone in life

- You want to cover the costs of your IHT bill using life insurance.

Get in touch and we’ll assess your circumstances and help you understand the type of trust that best suits your objectives.

5. Take out life insurance

Life insurance won’t reduce IHT, but it will mean that any tax your estate is liable for can be paid without eroding the value of your estate.

If you know your estate is likely to be subject to IHT, you can set up a life insurance policy that will pay a lump sum on your death to cover the expected tax bill.

Should you wish to use life insurance in this way, it’s crucial that the life insurance policy is placed in trust. Failure to do this will mean it will count as part of your estate and end up increasing the amount of IHT due.

Get in touch

We can help you to understand whether you have an IHT liability, and if so, what steps you can take to reduce or mitigate it.

If you would like to discuss your potential exposure to the tax and how you may be able to leave more money to your loved ones, email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note: The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

Levels and bases of, and relief from, taxation are subject to change.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.