April is Stress Awareness Month, which aims to raise awareness of the causes and potential coping strategies for feelings of stress. So, it’s an ideal time to get to grips with your anxieties about money.

Feeling overwhelmed by financial concerns and constantly worrying about money can be exhausting and it may affect your ability to enjoy life.

Whether you’re anxious about funding your retirement, or confused about how best to protect your wealth, taking practical steps to tackle your financial stress could boost your physical and mental health.

Read on to learn five simple ways to reduce your financial stress and start feeling happier.

1. Understand the causes of your financial stress

Identifying the triggers of your financial stress could be an important first step towards feeling calmer and more in control.

There might be many potential causes, such as worries about paying for later-life care or concerns about the performance of your investments if the market is volatile.

A lack of confidence and financial literacy could also be a factor. Indeed, the Financial Capability Survey has revealed that 39% of adults in the UK don’t feel confident managing their money.

To gain a clear picture of what’s causing your financial stress, you might find it helpful to write down your main concerns.

Talking to someone you trust, be that a family member, a friend, or a financial planner, could allow you to explore these concerns in more depth and prioritise which issues to tackle first.

One significant benefit of speaking to an impartial financial professional is that you won’t need to worry about the potential impact of your concerns on their wellbeing, as may be the case if you choose to speak to a family member.

A financial planner can provide a logical perspective based on their knowledge, experience, and the data you share with them.

For example, if you’re anxious about a short-term dip in the value of your investments, a financial planner could help you adopt a long-term view. They might also suggest opportunities for diversifying your portfolio to balance the level of risk you’re exposed to.

Once you have a clear understanding of what’s causing your financial stress, you can start taking action to reduce it.

2. Review your budget and create a financial plan

Understanding your financial situation by reviewing your budget and creating a plan for managing your money in the short-, medium-, and long-term, might help you feel more in control and reduce feelings of overwhelm.

You could start by looking at your income, expenditures, and debt. Are there any areas where you may be able to cut back on spending? Are you saving regularly? Reviewing your budget in this way might ensure that it aligns with your current circumstances and financial goals.

Additionally, creating a long-term financial plan could provide valuable guidance and reassurance. This in turn may reduce stress and allow you to focus on enjoying other areas of your life.

3. Build your emergency fund

Having to find money for an unexpected problem could be stressful. Conversely, building a contingency fund that you can fall back on may provide invaluable peace of mind.

Additionally, having an emergency fund might allow you to avoid or minimise expensive borrowing, such as using credit cards.

Experts suggest saving somewhere between three- and six-months’ expenses, although you may need more if you’re self-employed or your circumstances demand it.

Automating your savings can be a clever way to develop a regular and effortless saving habit. By setting up a recurring monthly transfer from your salary to your emergency fund, you could accumulate a nest egg to cover any unexpected costs that may arise.

4. Make sure you’re well protected

Putting sufficient protection in place to ensure that you and your family are taken care of if the worst happens could help to reduce your financial stress, both now and in the future.

Your emergency fund may cover short-term unexpected costs, but it might not be enough to provide a sustainable income if, for example, you become ill and unable to work.

On the other hand, financial protection tailored to your specific needs could help to pay for ongoing costs such as mortgage repayments, school fees, and other essential living costs.

The type and level of cover you need will depend on your unique circumstances. Life insurance, income protection, and critical illness cover could all provide valuable financial support during times of crisis.

Your insurance needs may also change over time, for example, if you move house or get married. So, it’s worth regularly reviewing your financial protection.

You might benefit from speaking to a financial planner about the options available and how to factor protection into your budget.

Read more: 3 important reasons to properly protect your financial plan

5. Seek professional financial advice

Whether you’re reviewing your budget or seeking out the best type of protection for your family, the choices available could be overwhelming – which may compound your financial stress.

Working with a financial planner can provide you with access to invaluable advice, information, and guidance.

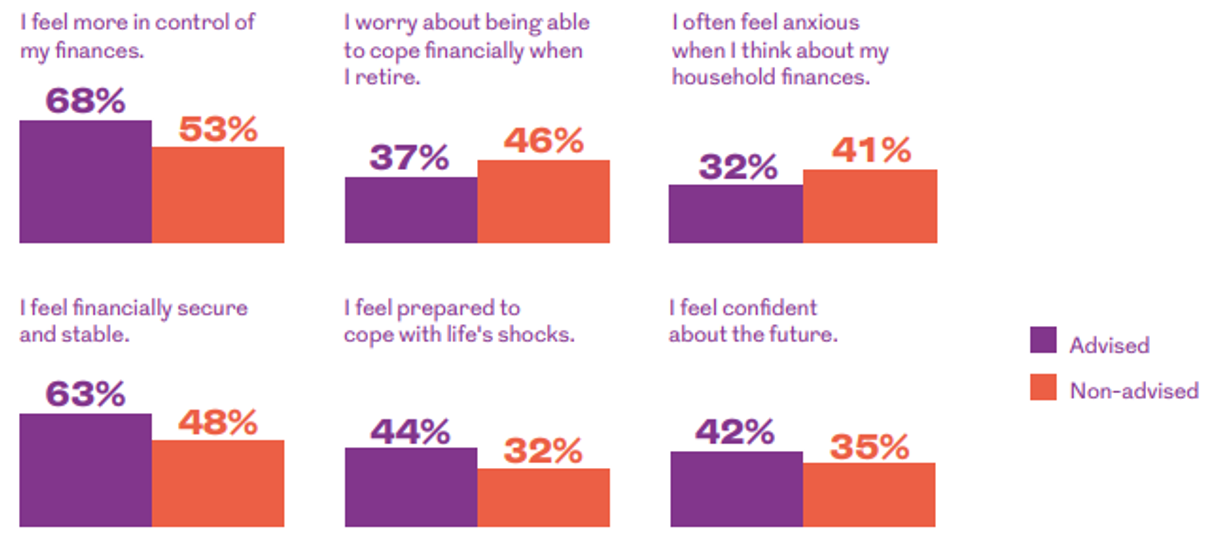

What’s more, research by Royal London has shown that consulting a financial professional regularly might boost mental wellbeing and reduce stress.

Those surveyed said that working with a financial planner helped them feel more in control of their finances, less anxious about money, and more financially secure and stable.

Get in touch

If you’d like to create a long-term plan that helps you feel more in control of your finances, we can help. Please email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

Blue Wealth Ltd is not responsible for the accuracy of the information contained within linked sites.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.

Note that life insurance plans typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Cover is subject to terms and conditions and may have exclusions. Definitions of illnesses vary from product provider and will be explained within the policy documentation.

No other dog would get away with sharing his bed (or taking his place in mine).

No other dog would get away with sharing his bed (or taking his place in mine).

The Bowers were also lucky enough to see the Northern Lights. Reliable sources said it was the best display seen for a couple of years. With specific conditions required for aurora borealis to happen, this was something even Rob couldn’t have planned for.

The Bowers were also lucky enough to see the Northern Lights. Reliable sources said it was the best display seen for a couple of years. With specific conditions required for aurora borealis to happen, this was something even Rob couldn’t have planned for. You may recall reading about

You may recall reading about  “Later in the year, we’re planning to have a bigger celebration with family and friends, giving everyone enough time to arrange to travel from other countries.

“Later in the year, we’re planning to have a bigger celebration with family and friends, giving everyone enough time to arrange to travel from other countries.