2025 has been a volatile year for global stock markets, driven by sticky inflation, conflicts in Ukraine and the Middle East, and President Trump’s trade tariffs – not to mention those DeepSeek, Tesla, and Nvidia headlines.

These market swings might have made you nervous about your investments.

However, seasoned investors don’t panic when the markets move up and down. Even if there’s a decline of 10% or more – a market correction – they keep their cool. Here’s why.

Market volatility is a normal part of long-term investing

If the value of your investments falls, it might be tempting to sell and limit your losses.

However, it’s important to understand that a degree of market volatility is inevitable.

Prices frequently rise and fall in response to:

- Political and world events

- Economic data

- Investor sentiment.

These movements might be unsettling, especially if there are significant declines, but they are part and parcel of investing.

Even significant declines – market corrections – are more common than you might think.

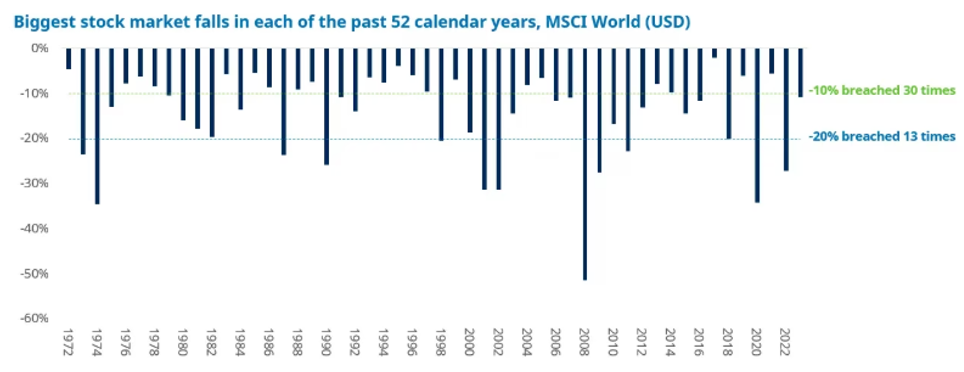

Figures published by Schroders reveal that between 1971 and 2023, stock market declines of 10% or more on the MSCI World Index occurred in the majority of years.

Source: Schroders

The graph shows that the market fell 10% or more in 30 out of 52 years, while declines of 20% or more happened in 13 years.

So, even headline-grabbing market dips, such as those reported in April 2025 following President Trump’s trade tariff announcement, are usually no cause for panic. They’re just part of the market’s natural rhythm.

Markets typically recover over the long term

Market volatility is both normal and temporary. Even the most significant corrections and crashes typically stabilise over time.

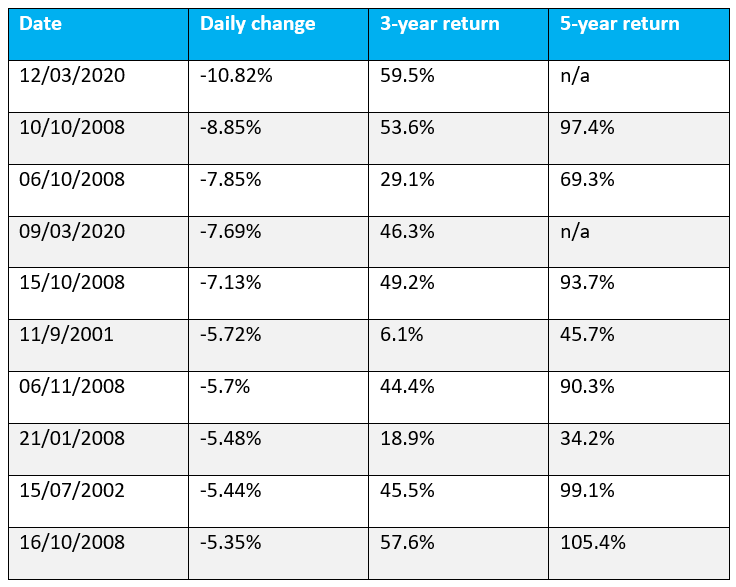

The chart below from Fidelity shows the 10 biggest one-day falls for the UK stock market, measured by the FTSE 100, as well as the subsequent three- and five-year returns.

Source: Fidelity

As you can see, over time, the markets recovered. As such, those who resisted the instinct to panic sell their shares and remained invested made gains in the long term.

The fluctuating market value of the technology company Nvidia further demonstrates the potential benefits of long-term investing.

On 27 January 2025, CNBC reported that Nvidia shares had fallen by 17%, resulting in a loss of almost $600 billion. This represents the biggest drop ever for a US company. However, by 9 July Forbes reported that the tech giant had made a huge comeback, becoming the first $4 trillion company ever.

So, had you sold your Nvidia shares after the January drop, you might have lost out on the subsequent gains.

While Nvidia stock fell again in the first week of November, its historic performance shows how impressively the market can recover over time.

4 ways to stay calm when the markets are volatile

If market volatility still makes you anxious about your investments, here are four tips for staying calm and avoiding emotional decisions.

1. Tune out the noise of market highs and corrections

In today’s technologically advanced world, you might be bombarded every day with investment-related news, whether through social media, the television, or even word of mouth.

Unfortunately, all this noise could make it harder to keep your emotions in check and avoid impulsive decisions, such as rushing to snap up an “unmissable” opportunity or sell shares that are falling in value.

That’s why experienced investors filter and limit the news sources they listen to and only check their portfolio every quarter.

2. Focus on your long-term goals

A cornerstone of effective investing is staying focused on your long-term goals, rather than the market.

As mentioned above, short-term market fluctuations are inevitable, and obsessively monitoring them could result in stress and poor choices.

Instead, anchoring your decisions to your goals could make market volatility less distracting and worrying.

It may also reduce the temptation to “follow the herd” – that is, to buy or sell shares based on other investors’ behaviours rather than your objectives.

Remember, you’re investing to make your life better, be that to retire early or to leave a meaningful legacy to loved ones. As such, an investment strategy that works for someone else might not be a good fit for you. That’s why your long-term goals need to be your priority.

3. Maintain a diversified portfolio

Spreading your wealth across different types of asset classes and geographical areas is known as diversification.

This strategy could help you stay calm because you’ll have peace of mind that no single event is likely to affect your entire portfolio. This is because different types of investments respond to different events. As such, some may fall in value while others make gains.

In contrast, if your portfolio is weighted heavily in one sector or region, this could leave you vulnerable to sudden market downturns.

4. Speak to a financial planner

Reviewing your investments periodically (or if your circumstances change) with a financial planner could help you avoid making emotional decisions. It could also ensure that the level of risk in your portfolio is effectively balanced and aligned with your goals.

Get in touch

If you struggle to remain calm and in control of your investments during periods of market volatility, we can provide the objective advice you need to stay on track to achieve your goals.

Please email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

Blue Wealth Ltd is not responsible for the accuracy of the information contained within linked sites.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Approved by Best Practice IFA Group: 25/11/25