With the Autumn Budget only a few months away, there has been growing speculation in the press about the possibility of tax increases.

You might have been keeping a close eye on this commentary and wondering how any potential changes could affect you. After all, higher taxes could mean that you have less disposable income to meet your ongoing needs and save for the future.

However, you may not realise that even if the chancellor makes no changes to existing tax rules, you might see your annual tax liabilities increase due to “stealth taxes”. These are indirect tax increases that often go unnoticed.

Keep reading to learn how these hidden taxes work and discover practical ways to protect your wealth.

Frozen Income Tax thresholds could push you into a higher tax bracket

Income Tax is a major source of revenue for the government. It is payable on most (although not all) types of income that exceed your Personal Allowance, which for most people is £12,570 in the 2025/26 tax year.

The amount of tax you’ll pay on earnings above the Personal Allowance depends on how much of your income falls within each of the following bands:

- Basic rate – 20% on earnings between £12,571 and £50,270.

- Higher rate – 40% on earnings between £50,271 and £125,140.

- Additional rate – 45% on earnings over £125,140.

Historically, these tax bands have increased each year in line with inflation and wage growth.

However, the Personal Allowance, basic- and higher-rate thresholds of Income Tax have not changed since April 2021. Moreover, the chancellor has confirmed that these thresholds will remain frozen until at least April 2028.

This is a classic example of a stealth tax. While there has been no direct increase in Income Tax rates, rising salaries and property prices could mean that more of your earnings fall into the higher tax brackets.

According to the Guardian, this “fiscal drag” means that the number of people paying higher-rate Income Tax is expected to increase by 500,000, to more than 7 million, in the 2025/26 tax year.

What’s more, the additional-rate threshold was reduced from £150,000 to £125,140 in April 2023, resulting in more people paying 45% tax on some of their income.

Static Inheritance Tax allowances could mean that your family pays more tax on your estate

If the value of your estate exceeds certain thresholds when you pass away, your beneficiaries might pay Inheritance Tax (IHT) – the standard rate is 40% in 2025/26 – on a portion of your wealth.

IHT thresholds have been frozen until at least April 2030:

- The “nil-rate band” is the amount you can pass on before IHT is payable. This has been frozen at £325,000 since April 2009.

- The “residence nil-rate band” – an additional allowance that may be available if you pass on your main home to your children or grandchildren – has remained at £175,000 since April 2020.

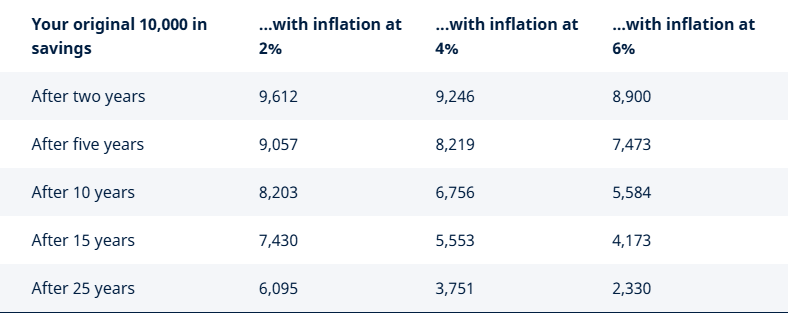

Unfortunately, this failure to keep up with inflation could mean that your family faces a larger IHT bill.

Imagine that your estate was worth £300,000 in 2009. This falls below the nil-rate band, so your beneficiaries would likely not have paid any IHT. Now fast forward to 2025.

According to the Bank of England’s inflation calculator, your estate could now be worth over £481,000. As such, around £156,000 falls beyond the nil-rate band and could trigger an IHT charge (assuming that you cannot benefit from the residence nil-rate band).

Put simply, while the government has not increased the rate of IHT, the freeze on thresholds means that more estates are liable for IHT or facing a higher bill than they might have previously.

Indeed, the latest figures released by HMRC reveal that gross HMRC Tax and NICs receipts for April to August 2025 were £22.1 billion higher than the same period last year.

3 clever ways to protect your wealth from stealth taxes

Fortunately, there are some practical steps you can take to protect your wealth from stealth taxes. Here are three:

1. Rethink your pension contributions

You could reduce your taxable income and potentially avoid moving into a higher tax bracket by paying more into your workplace and private pensions each month.

As such, increasing your pension contributions may help to reduce your tax liabilities while also boosting your retirement savings.

It’s also worth asking your employer if they offer, or would consider offering, a salary sacrifice scheme. This would allow you to exchange or “sacrifice” part of your earnings for other benefits, such as pension contributions.

Your Income Tax and National Insurance contributions would then be calculated based on your reduced salary. As a result, your take-home pay may increase while the amount going into your pension remains the same.

2. Top up your ISAs

In the 2025/26 tax year, you can contribute up to £20,000 in total across your ISA accounts without incurring Income Tax or Capital Gains Tax on any interest or returns. This annual allowance will reset on 6 April 2026 – you can’t carry any of this allowance over into the new tax year, so if you don’t use it, you lose it.

As such, topping up your ISAs could shield more of your wealth from tax and help you maximise tax-efficient growth.

In contrast, any interest you earn on savings held outside an ISA wrapper may be taxed at your marginal rate if you exceed certain thresholds. So, if the frozen Income Tax thresholds have pushed you into a higher band, ISAs could be a valuable tool for reducing the tax you pay on savings interest.

3. Make use of Inheritance Tax gifting allowances and exemptions

Passing on some of your wealth during your lifetime by using IHT gifting allowances and exemptions could lower the value of your estate and minimise future IHT liabilities.

For example, the annual exemption allows you to give away gifts worth up to £3,000 each year (2025/26), without them being added to your estate for IHT purposes.

If rising estate valuations and frozen tax thresholds are likely to increase the IHT bill on your estate, giving while living in this way could be a useful way to protect some of your wealth from stealth taxes.

Get in touch

If you think you might be affected by any of the stealth taxes mentioned above, we can help you keep your wealth as tax-efficient as possible.

Please email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The content of this newsletter is offered only for general informational and educational purposes. It is not offered as, and does not constitute, financial advice.

Blue Wealth Ltd is not responsible for the accuracy of the information contained within linked sites.

Blue Wealth Ltd is an appointed representative of Best Practice IFA Group Ltd, which is authorised and regulated by the Financial Conduct Authority.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning, or tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts

Workplace pensions are regulated by The Pensions Regulator.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Approved by Best Practice IFA Group: 18/09/2025