According to data from the Financial Conduct Authority (FCA), 15.6 million UK adults have investible assets of £10,000 or more. Of these, 37% hold their assets entirely in cash, and a further 18% hold more than 75% in cash.

With current stock market uncertainties caused by the war in Ukraine and the economic turbulence of rising inflation and interest rates, it’s easy to see how some investors may feel safer to leave their money in the bank.

Retreating to cash might provide some comfort in turbulent times

Since cash is easily accessible, it’s great for your emergency fund. However, while retreating to cash might provide some comfort – especially during turbulent times – holding on to too much cash could actually be bad for your long-term financial health.

3 reasons not to hold too much cash in the bank

Here are three reasons to avoid holding too much of your money as cash.

1. Other assets can provide greater long-term returns

Numerous studies have proved that, over time, returns on assets such as equities far outweigh those you see from cash.

The 2019 Barclays Equity Gilt Study compared the performance of £100 invested in cash, bonds, and equities between 1899 and 2018. The report revealed that:

- £100 invested in cash in 1899 was worth just over £20,000 in 2018

- £100 invested in gilts in 1899 was worth close to £42,000 in 2018

- £100 invested in equities in 1899 was worth around £2.7 million in 2018.

While few of us are likely to want to invest for more than a century, the same study showed that even with a shorter investment term, equities will still outperform cash.

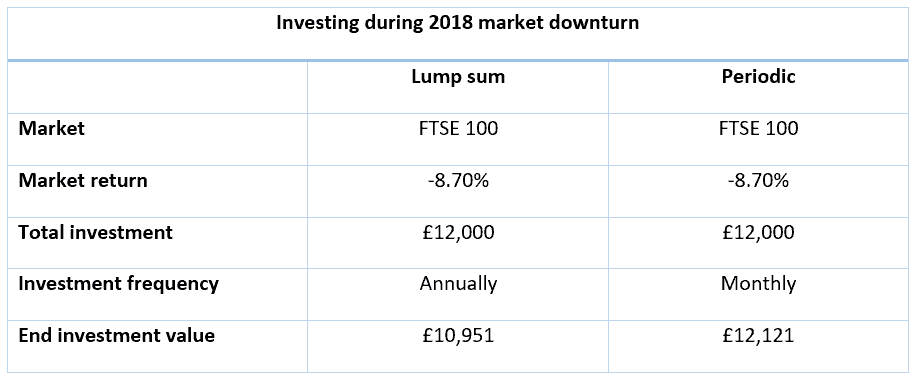

Also, as long as the time horizon is long enough, history shows that the timing of a new investment is relatively unimportant when it comes to enjoying long-term returns.

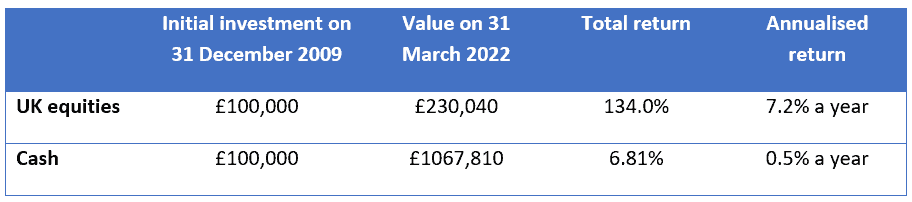

The tables below compare the returns of investing in the UK stock market (as represented by the FTSE All Share Index) with dividends re-invested and the returns of investing in cash deposits with interest re-invested.

Since the beginning of 2000 to 31 March 2022 (just over 21 years)

Since the beginning of 2010 to 31 March 2022 (just over 11 years)

Source: FE fundinfo – data as at 31 March 2022.

Bear in mind, the value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

The returns in the two tables above are very different. This is because the longer, first period includes the two bear markets. Following the “dotcom bust” in 2000, UK equities fell by 48% between September 2000 and March 2003.

Similarly, UK equities fell by 46% between October 2007 and March 2009 during the 2008 financial crisis. However, despite these two significant declines, equities have still outperformed cash deposits by more than 100% since the beginning of the century.

Of course, both periods also include the 35% fall in UK equities between January and March 2000 as the Covid pandemic took hold.

2. Savings rates struggle to beat inflation

According to data from Moneyfacts, the best rate of interest you can currently find from an easy access savings account is 1.67%. With inflation at 10.1%, if your money is in an instant access account, returns are not keeping up with rises in the cost of living.

Many accounts pay even less.

Even if you somehow manage to find a fixed-rate bond or similar limited access account that pays a higher rate, there’s slim chance that it will keep up with inflation. The problem with this is that if the returns you get on your savings are lower than the inflation rate, your money is losing value in real terms.

This is another excellent reason not to hold too much cash.

Read more: What is inflation and what does it mean for you and your wealth?

3. You could be taxed on interest

While we recommend you keep an emergency fund in an easy access savings account so you always have available cash should you need it, avoid holding more than you need.

Generally, it’s wise to have between three and six months net income for a “rainy day” fund. With average monthly earnings in the UK around £2,000, that could mean having an emergency fund of £12,000 or more.

If you’d like to know more about the importance of maintaining a “rainy day” fund, watch this video from Mason on LinkedIn.

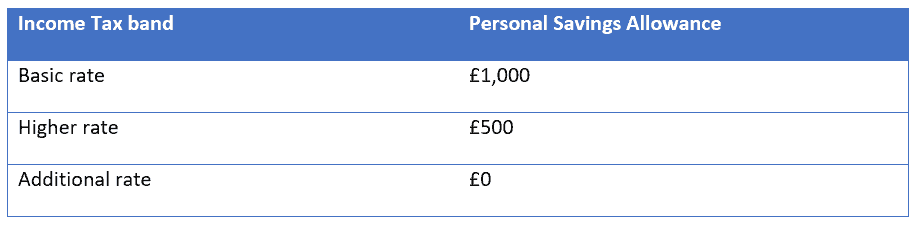

Cash savings are protected by the FSCS up to £85,000. If you hold more than this amount in any one account and the financial institution holding your funds fails, you could lose everything over this threshold amount.

Large cash savings can also attract tax on the interest you make. Your Personal Savings Allowance is based on the rate of Income Tax you pay.

Source: Gov.uk

If you are a basic-rate taxpayer, you’ll pay tax on interest over £1,000. For higher-rate taxpayers, the threshold is halved to £500.

Get in touch

If you’d like to talk to us about the balance of your assets, or you’re concerned about inflation affecting your cash savings, please get in touch. Email hello@bluewealth.co.uk or call us on 0117 332 0230.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Naomi is our new trainee paraplanner. Arriving from another firm in Bristol, here she tells us a bit more about what she’s been up to since joining the team at Blue Wealth.

Naomi is our new trainee paraplanner. Arriving from another firm in Bristol, here she tells us a bit more about what she’s been up to since joining the team at Blue Wealth.

What is your background, can you tell us a bit about your journey to becoming a financial planner?

What is your background, can you tell us a bit about your journey to becoming a financial planner?